El Segundo, CA —Worldwide semiconductor market revenue is on track to achieve a 9.4% expansion this year, with broad-based growth across multiple chip segments driving the best industry performance since 2010.

Global revenue in 2014 is expected to total $353.2 billion, up from $322.8 billion in 2013, according to a preliminary estimate from IHS Technology (NYSE: IHS). The nearly double-digit-percentage increase follows respectable growth of 6.4% in 2013, a decline of more than 2.0% in 2012 and a marginal increase of 1.0% in 2011. The performance in 2014 represents the highest rate of annual growth since the 33% boom of 2010.

“This is the healthiest the semiconductor business has been in many years, not only in light of the overall growth, but also because of the broad-based nature of the market expansion,” said Dale Ford, vice president and chief analyst at IHS Technology. “While the upswing in 2013 was almost entirely driven by growth in a few specific memory segments, the rise in 2014 is built on a widespread increase in demand for a variety of different types of chips. Because of this, nearly all semiconductor suppliers can enjoy good cheer as they enter the 2014 holiday season.”

More information on this topic can be found in the latest release of the Competitive Landscaping Tool from the Semiconductors & Components service at IHS.

Widespread growth

Of the 28 key subsegments of the semiconductor market tracked by IHS, 22 are expected to expand in 2014. In contrast, only 12 subsegments of the semiconductor industry grew in 2013.

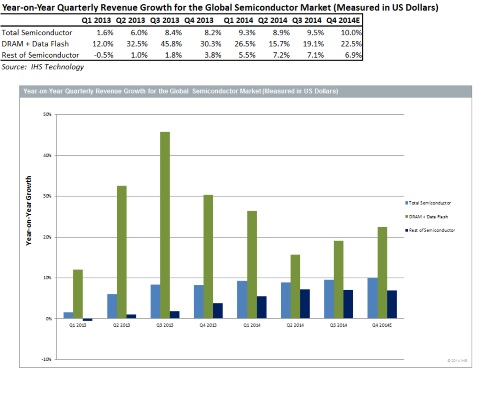

Last year, the key drivers of the growth of the semiconductor market were dynamic random access memory (DRAM) and data flash memory. These two memory segments together grew by more than 30% while the rest of the market only expanded by 1.5%.

This year, the combined revenue for DRAM and data flash memory is projected to rise about 20%. However, growth in the rest of the market will swell by 6.7% to support the overall market increase of 9.4%.

In 2013, only eight semiconductor subsegments grew by 5% or more and only three achieved double-digit growth. In 2014, over half of all the subsegments — i.e., 15 — will grow by more than 5% and eight markets will grow by double-digit percentages.

This pervasive growth is delivering general benefits to semiconductor suppliers, with 70% of chipmakers expected to enjoy revenue growth this year, up from 53% in 2013.

The figure above presents the growth of the DRAM and data flash segments compared to the rest of the semiconductor market in 2013 and 2014.

Semiconductor successes

The two market segments enjoying the strongest and most consistent growth in the last two years are DRAM and light-emitting diodes (LEDs). DRAM revenue will climb 33% for two years in a row in 2013 and 2014. This follows often strong declines in DRAM revenue in five of the last six years.

The LED market is expected to grow by more than 11% in 2014. This continues an unbroken period of growth for LED revenues stretching back at least 13 years.

Major turnarounds are occurring in the analog, discrete and microprocessor markets as they will swing from declines to strong growth in every subsegment. Most segments will see their growth improve by more than 10%, compared to the declines experienced in 2013.

Furthermore, programmable logic device (PLD) and digital signal processor (DSP) application-specific integrated circuits (ASICs) will experience dramatic improvements in growth. PLD revenue in 2014 will grow by 10.2% compared to 2.1% in 2013, and DSP ASICs will rise by 3.8% compared to a 31.9% collapse in 2013.

Moving on up

Among the top 20 semiconductor suppliers, MediaTek and Avago Technologies attained the largest revenue growth and rise in the rankings in 2014. Both companies benefited from significant acquisitions.

MediaTek is expected to jump up five places to the 10th rank and become the first semiconductor company headquartered in Taiwan to break into the Top 10. Avago Technologies is projected to jump up eight positions in the rankings to No. 15.

The strongest growth by a semiconductor company based purely on organic revenue increase is expected to be achieved by SK Hynix, with projected growth of nearly 23%.

No. 13-ranked Infineon has announced its plan to acquire International Rectifier. If that acquisition is finalized in 2014 the combined companies would jump to No. 10 in the overall rankings and enjoy 16% combined growth.

The table attached presents the preliminary IHS ranking of the world’s top 20 semiconductor suppliers in 2013 and 2014 based on revenue.

Troubles for consumer electronics and Japan

Semiconductor revenue in 2014 will grow in five of the six major semiconductor application end markets, i.e. data processing, wired communications, wireless communications, automotive electronics and industrial electronics. The only market segment experiencing a decline will be consumer electronics. Revenue will expand by double-digit percentages in four of the six markets.

Japan continues to struggle, and is the only worldwide region that will see a decline in semiconductor revenues this year. The other three geographies — Asia-Pacific, the Americas and the Europe, Middle East and Africa (EMEA) region — will see healthy growth. The world will be led by led by Asia-Pacific which will post an expected revenue increase of 12.5%.

Advertisement

Learn more about IHS iSuppli