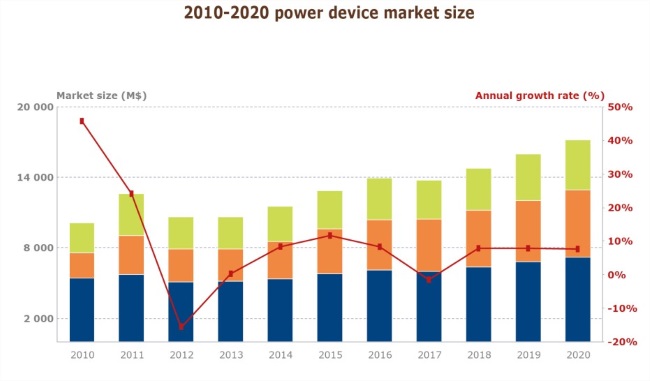

A new report about the fiscal health of the power electronics industry from Yole Developpement offers some good news. The report, which will be available March 20, 2015, says that 2014 was a year of recovery after two stagnant years. The research says the power semiconductor device market grew 8.4% in 2014 to $11.5B. Even better, the outlook for the next five years is positive, driven by EV and HEV sales, although I wonder what affect the recently lower cost of oil will have on semiconductor growth.

Not surprisingly, IGBTs will lead the growth will lead the growth at 10.3% CAGR from 2014 to 2020. The report says that the excellent growth of IGBTs is due to their improved efficiency and thermal conductivity management. Additionally, wide band gap devices (SiC, GaN) will also drive growth and represent about 5% of the overall dollar amount in the market by 2020.

The report also presents data for different applications such as photovoltaics, wind turbines, transmission and distribution, EV/HEV, rail traction, uninterruptible power supplies and motor drives, as well as from different value chain levels, covering wafers, devices, and inverters. Technologically, MOSFETs and IGBTs are and will continue to be the devices in greatest demand, covering low and medium-high voltage applications respectively. New technologies have appeared in the last decade, such as Super Junction MOSFETs, which have brought the MOSFET family into higher voltage segments up to 900 V, with better performance. In terms of power packaging, ongoing evolution is driven particularly by the EV/HEV industry.

The research also says that the introduction of SiC into other high voltage segments, such as wind and high-voltage direct current grids is also inevitable. But the big boost for these new markets should arrive with the implementation of SiC devices in electric cars’ traction systems. GaN systems are still less present on the market. Some consumer applications, such as laptop chargers, and just-announced PV inverters are going to be the first segments incorporating GaN. Several system manufacturers are also developing further SiC and/or GaN device-based prototypes and thus the next 5 years are going to be decisive for WBG devices’ introduction into different markets.

Interestingly, the report says that the supply chain is evolving. It says that the power electronics supply chain is mostly application- and local market-dependent. European and American players will prioritize horizontal integration, keeping proven expertise in a specific level of the value chain. Therefore, partnerships and joint-ventures will be preferred. This report analyzes the major mergers and acquisitions of 2014, for instance International Rectifier’s acquisition by Infineon, in order to understand their context and purpose.

Some system manufacturers, such as Tesla or BYD developing their own power electronics and energy management systems for traction, chargers and batteries in order to offer extended added-value. Asian companies will prefer to expand vertically in order to be fully integrated and optimize the costs. Japanese players are already vertically integrated and involved in multiple applications simultaneously to benefit from their technologies across different markets. Chinese players are developing this vertical integration in order to create major market leaders in each application segment such as SunGrow in PV, GoldWind in wind and BYD in EV/HEV. This report focusses especially on the details of the Chinese market, which is driven by Chinese Government policies. In this changing environment, western and Japanese players need to bring high added-value solutions to be able to compete with Chinese companies. The report includes a complete section on main players’ strategies.

For more information : http://www.i-micronews.com/power-electronics-report/product/status-of-power-electronics-industry-2015.html

Advertisement