By Barbara Jorgensen and Gina Roos

Yageo Corp.’s acquisition of Kemet Corp. will unite two leading component makers into a $3 billion powerhouse in the interconnect, passives and electromechanical (IP&E) market. The move will expand both companies’ global footprint, market penetration and product portfolios.

“Together with Yageo, we will have an enhanced global footprint and be better able to partner with longstanding blue-chip customers worldwide through a combined 42 manufacturing plants and 14 dedicated R&D centers with an increased presence and attractive high growth segments and applications,” Kemet CEO Bill Lowe told analysts. “This includes consumer electronics as well as in the high-end automotive, industrial, aerospace, telecom, and medical sectors.”

Bill Lowe, Kemet CEO (Image: Kemet Corp.)

Taiwan-based Yageo is now positioned to be a one-stop shop of passive electronic components. The product portfolio includes polymer, tantalum, ceramic, film and electrolytic capacitors; chip resistors, circuit protection as well as magnetics, sensors, and actuators.

“Once again Yageo proves their excellence at acquiring companies anywhere in the world with an eye on technology and customer access,” said Dennis Zogbi, president, Paumanok. “It also demonstrates Yageo’s ability to purchase companies today that will create great value for shareholders in the next upward cycle.”

The merger was announced just as Kemet came off a rough fiscal quarter. Revenue for Q2 2020 was down 6.3% to $327.4 million compared to Q2 last year of $349.2 million. GAAP net income was negative $15.3 million or $0.26 per share loss for the quarter compared to GAAP net income of $37.1 million or $0.63 per diluted share for the quarter ended September 30, 2018. “This decline was driven by one-time items relating to litigation settlements,” said Greg Thompson, executive vice president and chief financial officer.”

Kemet reported a one-time item related to an antitrust settlement agreement in which Kemet and more than 20 other capacitor manufacturers and subsidiaries are defendants in a purported class-action complaint relating to the sale of capacitors in the United States, said Thompson. Kemet has agreed to pay an aggregate of $62 million; $10 million within 30 calendar days of the date of the settlement, and the remaining $52 billion within 12 months, said Thompson.

Anatomy of a merger

Kemet has historically been a fiscally conservative company that has weathered numerous industry cycles. The company did not actively seek a merger partner, said Lowe. The company was approached earlier in the calendar year, and under fiduciary responsibilities, it was required to consider the offer. Kemet executives were reluctant to share additional details of the process until it has issued a proxy statement in early 2020.

Kemet, like many component makers, is also dealing with inventory issues following a two-year shortage of capacitors. Inventory is now plentiful in the supply chain for many components that were in short supply, so prices and margins both are under pressure.

Kemet has made some structural changes over the past several years to improve profitability, including focusing on value-added applications for the ceramics product line, vertically integrating the tantalum business to improve cost, and focusing on the newer polymer technology, as well as acquiring NEC Tokin to expand its product offering.

Recommended

Passive component shortages drive new supply strategies at Kemet

“This quarter's results continue to highlight that these structural changes make us a different company today than we were several years ago as we demonstrate continuing strong sustainable profitability performance in spite of the slowdown in the electronics industry,” Thompson said.

“Kemet is one of the leading manufacturers of capacitors and the world’s largest tantalum capacitor manufacturer. Its products, in addition to tantalum capacitors, include multi-layer ceramic, solid and electrolytic aluminum and film & paper capacitors as well as electromagnetics, sensors & actuators acquired from the NEC Tokin acquisition,” analyst Matt Sheerin of Stifel said in a research note. “In the last several years, we believe, Kemet has undergone an impressive turnaround, enduring ill-timed acquisitions, balance-sheet woes, the severe downturn, and a recapitalization. The company completed the NEC Tokin acquisition on extremely favorable terms, generating accretive earnings and a solid balance sheet. With margins now at multiyear highs and the balance sheet in strong shape, the long-term story seems compelling.”

A couple of the biggest benefits for Yageo is access to Kemet’s presence in Japan through Kemet’s NEC Tokin acquisition, and advanced products in high-reliability-type markets, including automotive, 5G networking, robotics, automation, and industrial segments.

Kemet will be able to scale its business in Greater China and ASEAN regions through Yageo’s channels. The combined companies will have 42 manufacturing plants and 14 dedicated research and development (R&D) centers.

“Because of Kemet’s and Yageo’s complimentary product offerings, the combined company will be an industry leader in the $28 to $32 billion passive components industry and serve as a one-stop provider of a robust portfolio of polymer, tantalum, ceramic, film, and electrolytic capacitors; chip resistors, circuit protection, as well as magnetic sensors and actuators with revenue of approximately $3 billion,” said Lowe.

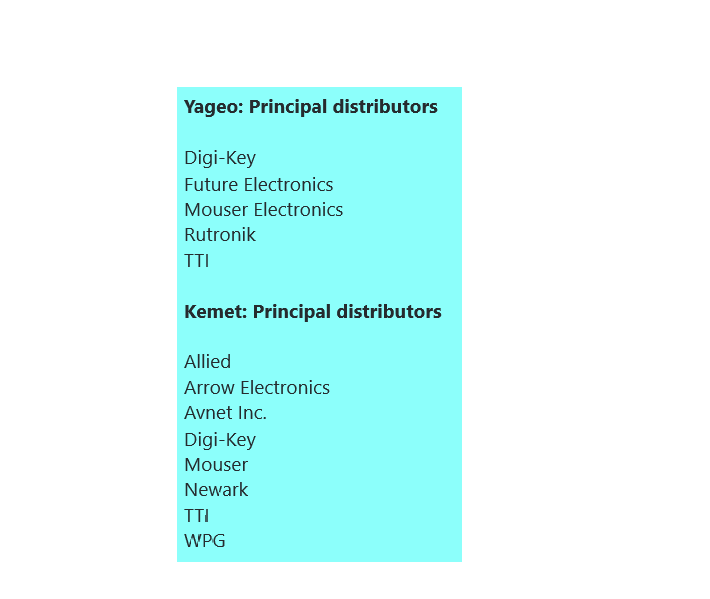

The merger, however, has prompted some uncertainty among customers and distributors. If Yageo and Kemet have product lines that overlap, one line will likely be discontinued. This is a problem for customers that have designed that line into their products, especially long-lifecycle equipment.

A merger also brings together two disparate distribution rosters. If Yageo and Kemet have distributors in common — which they do — those partners likely will stay intact. Distributors that carry only one line may gain the combined product portfolio – or they may be dropped.

Finalization of the merger is contingent on meeting antitrust and other regulatory approvals in the United States (including from the Committee on Foreign Investment in the United States (“CFIUS”), and other jurisdictions including China and Taiwan (including foreign investment approval by the Investment Commission, Ministry of Economic Affairs, Taiwan).

Lowe does not anticipate any regulatory hurdles due to customers in the military, aerospace, and industrial markets, and expects Kemet to file for CFIUS approval over the next 60 days.

“We do have to file for CFIUS approval. We're not expecting that to be a particular issue, but we do have to file for that approval, and that could take six to seven months to get that through,” he said. “At one time or the other we'll have various components that are considered to be ITAR-related, but not on a consistent basis. So, it shouldn't be a major material issue to deal with. Our expectations are that we will work through that.”

The article originally published on sister publication EPSNews.

Advertisement

Learn more about Electronic Products Magazine